WHAT ARE FINANCIAL STATEMENTS? A CASE STUDY

Pat was applying for a bank loan to start her new business, Nutrivite, a retail store selling nutritional supplements, vitamins, and herbal remedies. She described her concept to Kim, a loan officer at the bank.

Kim: How much money will you need to get started?

Pat: I estimate $80,000 for the beginning inventory, plus $36,000 for store signs, shelves, fixtures, counters, and cash registers, plus $24,000 working capital to cover operating expenses for about two months. That’s a total of $140,000 for the startup.

Kim: How are you planning to finance the investment of the $140,000?

Pat: I can put in $100,000 from my savings, and I’d like to borrow the remaining $40,000 from the bank.

Kim: Suppose the bank lends you $40,000 on a one-year note, at 15% interest,secured by a lien on the inventory. Let’s put together projected financial statements from the figures you gave me. Your beginning balance sheet would look like what you see on my computer screen:

The left side shows Nutrivite’s investment in assets. It classifies the assets into “current” (which means turning into cash in a year or less) and “noncurrent” (not turning into cash within a year). The right side shows how the assets are to be financed: partly by the bank loan and partly by your equity as the owner. Pat: Now I see why it’s called a “balance sheet.” The money invested in assets must equal the financing available—its like the two sides of a coin. Also, I see why the assets and liabilities are classified as “current” and “noncurrent”—the bank wants to see if the assets turning into cash in a year or less will provide enough cash to repay the one-year bank loan. Well, in a year there should be cash of $104,000. That’s enough cash to pay off more than twice the $40,000 amount of the loan. I guess that guarantees approval of my loan! Kim: We’re not quite there yet. We need some more information. First, tell me, how much do you expect your operating expenses will be? Pat: For year 1, I estimate as follows:

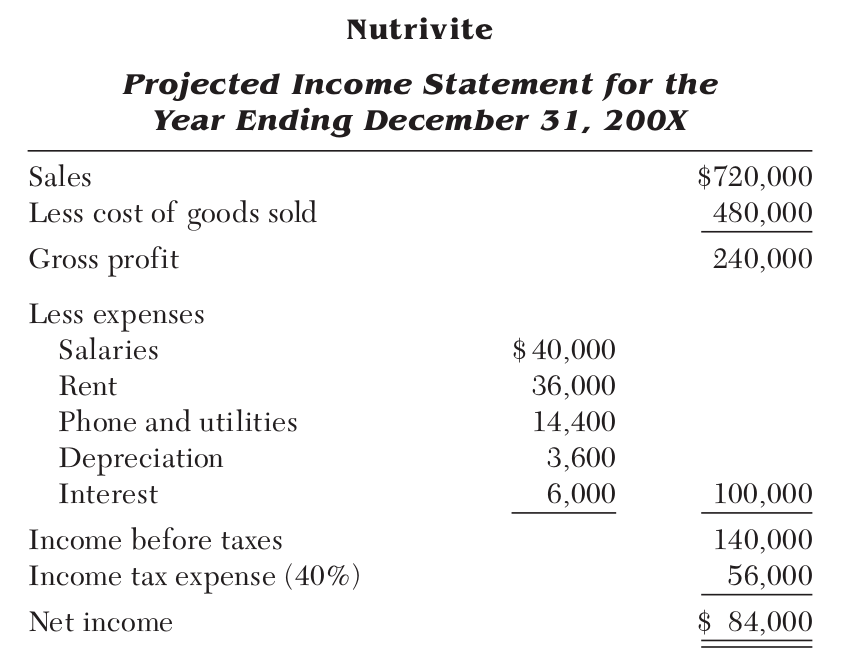

Kim: We also have to consider depreciation on the store equipment. It probably has a useful life of 10 years. So each year it depreciates by 10% of its cost of $36,000. That’s $3,600 a year for depreciation. So operating expenses must be increased by $3,600 a year, from $96,400 to $100,000. Now, moving on, how much do you think your sales will be this year?

Pat: I’m confident that sales will be $720,000 or even a little better. The wholesale cost of the items sold will be $480,000, giving a markup of $240,000—which is 33 1 ⁄ 3 % on the projected sales of $720,000.

Kim: Excellent! Let’s organize this information into a projected income statement. We start with the sales, then deduct the cost of the items sold to arrive at the gross profit. From the gross profit we deduct your operating expenses, giving us the income before taxes. Finally we deduct the income tax expense in order to get the famous “bottom line,” which is the net income. Here is the projected income statement shown on my computer screen:

Pat, this looks very good for your first year in a new business. Many business startups find it difficult to earn income in their first year. They do well just to limit their losses and stay in business. Of course, I’ll need to carefully review all your sales and expense projections with you, in order to make sure that they are realistic. But first, do you have any questions about

the projected income statement?

Pat: I understand the general idea. But what does “gross profit” mean?

Kim: It’s the usual accounting term for sales less the amount that your suppliers charged you for the goods that you sold to your customers. In other words, it represents your markup from the wholesale cost you paid for goods and the price for which you sold those goods to your customers. It is called “gross profit” because your operating expenses have to be deducted from it. In accounting, the word gross means “before deductions.” For example “gross sales” means sales before deducting goods returned by customers. Sales after deducting goods returned by customers are referred to as “net sales.” In accounting, the word net means “after deductions.” So “gross profit” means income before deducting operating expenses. By the same token, “net income” means income after deducting operating expenses and income taxes. Now, moving along, we are ready to figure out your projected balance sheet at the end of your first year in business. But first I need to ask you how much cash you plan to draw out of the business as your compensation?

Pat: My present job pays $76,000 a year. I’d like to keep the same standard of compensation in my new business this coming year.

Kim: Let’s see how that works out after we’ve completed the projected balance sheet at the end of year 1. Here it is on my computer screen:

Let’s go over this balance sheet together, Pat. It has changed compared to the balance sheet as of January 1. On the Liabilities and Equity side of the balance sheet, the Net Income of $84,000 has increased Capital to $184,000 (because earning income adds to the owner’s Capital), and deducting Drawings of $76,000 has reduced Capital to $108,000 (because Drawings take Capital out of the business). On the asset side, notice that the Equipment now has a year of depreciation deducted, which writes it down from the original $36,000 to a net (there’s that word net again) $32,400 after depreciation. The Equipment had an expected useful life of 10 years, now reduced to a remaining life of 9 years. Last but not least, notice that the

Cash has increased by $11,600 from $24,000 at the beginning of the year to $35,600 at year-end. This leads to a problem: The Bank Loan of $40,000 is due for repayment on December 31. But there is only $35,600 in Cash available on December 31. How can the Loan be paid off when there is not enough Cash to do so?

Pat: I see the problem. But I think it’s bigger than just paying off the loan. The business will also need to keep about $25,000 cash on hand to cover two months operating expenses and income taxes. So, with $40,000 to repay the loan plus $25,000 for operating expenses, the cash requirements add up to $65,000. But there is only $35,600 cash on hand. This leaves a cash shortage of almost $30,000 ($65,000 less $35,600). Do you think that will force me to cut down my drawings by $30,000, from $76,000 to $45,000? Here I am opening my own business, and it looks as if I have to go back to what I was earning five years ago!

Kim: That’s one way to do it. But here’s another way that you might like better. After your suppliers get to know you and do business with you for a few months, you can ask them to open credit accounts for Nutrivite. If you get the customary 30-day credit terms, then your suppliers will be financing one month’s inventory. That amounts to one-twelfth of your $480,000 annual

cost of goods sold, or $40,000. This $40,000 will more than cover the cash shortage of $30,000.

Pat: That’s a perfect solution! Now, can we see how the balance sheet would look in this case?

Kim: Sure. When you pay off the Bank Loan, it vanishes from the balance sheet. It is replaced by Accounts Payable of $40,000. Then the balance sheet looks like this:

Now the cash position looks a lot better. But it hasn’t been entirely solved: There is still a gap between the Accounts Payable of $40,000 and the Cash of $35,600. So you will need to cut your drawings by about $5,000 in year 1. But that’s still much better than the cut of $30,000 that had seemed necessary before. In year 2 the Bank Loan will be gone, so the interest expense of $6,000 will be saved. Then you can use $5,000 of this saving to restore your drawings back up to $76,000 again.

Pat: That’s good news. I’m beginning to see how useful projected financial statements are for business planning. Can we look at the revised projected balance sheet now?

Kim: Of course. Here it is:

As you can see, Cash is increased by $5,000 to $40,600—which is sufficient to pay the Accounts Payable of $40,000. Drawings is decreased by $5,000 to $71,000, which provided the $5,000 increase in Cash. Pat: Thanks. That makes sense. I really appreciate everything you’ve taught me about financial statements.

Kim: I’m happy to help. But there is one more financial statement to discuss. Besides the balance sheet and income statement, a full set of financial statements also includes a cash f low statement. Here is the projected cash f low statement:

Pat, do you have any questions about this Cash Flow Statement?

Pat: Actually, it makes sense to me. I realize that there are only two sources that a business can tap in order to generate cash: internal (by earning income) and external (by obtaining cash from outside sources, such as bank loans). In our case the internal sources of cash are represented by the “Cash from Operations” section of the Cash Flow Statement, and the external

sources are represented by the “Cash from Financing” section. It happens that the “Cash from Financing” is negative because no additional outside financing is received for the year 200X, but cash payments are incurred for Drawings and for repayment of the Bank Loan. I also understand that there are no “Uses of Cash” because no extra Equipment was acquired. In addi-

tion, I can see that the Total Sources of Cash less the Total Uses of Cash must equal the Increase in Cash, which in turn is the Cash at the end of the year less the Cash at the beginning of the year. But I am puzzled by the “Cash from Operations” section of the Cash Flow Statement. I can understand that earning income produces Cash. However why do we add back De-

preciation to the Net Income in order to calculate Cash from Operations?

Kim: This can be confusing, so let me explain. Certainly Net Income increases Cash, but first an adjustment has to be made in order to convert Net Income to a cash basis. Depreciation was deducted as an expense in figuring Net Income. So adding back depreciation to Net Income just reverses the charge for depreciation expense. We back it out because depreciation is not a cash outf low. Remember that depreciation represents just one year’s use of the Equipment. The cash outf low for purchasing the Equipment was incurred back when the Equipment was first acquired and amounted to $36,000. The Equipment cost of $36,000 is spread out over the 10-year life of the Equipment at the rate of $3,600 per year, which we call Depreciation expense. So it would be double counting to recognize the $36,000 cash outf low for the Equipment when it was originally acquired and then to recognize it a second time when it shows up as Depreciation expense. We do not write a check to pay for Depreciation each year, because it is not a cash outf low.

Pat: Thanks. Now I understand that Depreciation is not a cash outf low. But I don’t see why we also added back the Increase in Current Liabilities to the Net Income to calculate Cash from Operations. Can you explain that?

Kim: Of course. The increase in Current Liabilities is caused by an increase in Accounts Payable. These Accounts Payable are amounts owed to our suppliers for our purchases of goods for resale in our business. Purchasing goods for resale from our suppliers on credit is not a cash outf low. The cash outf low only occurs when the goods are actually paid for by writing out checks to our suppliers. That is why we added back the Increase in Current Liabilities to the Net Income in order to calculate Cash from Operations. In the future, the Increase in Current Liabilities will, in fact, be paid in cash. But that will take place in the future and is not a cash outf low in this year. Going back to the Cash Flow Statement, notice that it ties in neatly with our balance sheet amount for Cash. It shows how the Cash at the beginning of the year plus the Net Cash Increase equals the Cash at the end of the year.

Pat: Now I get it. Am I right that you are going to review my projections and then I’ll hear from you about my loan application?

Kim: Yes, I’ll be back to you in a few days. By the way, would you like a printout of the projected financial statements to take with you?

Pat: Yes, please. I really appreciate your putting them together and explaining them to me. I picked up some financial skills that will be very useful to me as an aspiring entrepreneur.

Frequently Asked Questions

Recommended Posts:

- THE PROCESS OF IDENTIFYING NONRECURRING ITEMS

- NONRECURRING ITEMS IN THE INCOME STATEMENT

- NONRECURRING ITEMS IN THE STATEMENT OF CASH FLOWS

- NONRECURRING ITEMS IN THE INVENTORY DISCLOSURES OF LIFO FIRMS

- NONRECURRING ITEMS IN THE INCOME TAX NOTE

- NONRECURRING ITEMS IN THE OTHER INCOME AND EXPENSE NOTE

- NONRECURRING ITEMS IN MANAGEMENTS DISCUSSION AND ANALYSIS (MD&A)

- NONRECURRING ITEMS IN OTHER SELECTED NOTES

- EARNINGS ANALYSIS AND OTHER COMPREHENSIVE INCOME

- SUMMARIZING NONRECURRING ITEMS AND DETERMINING SUSTAINABLE EARNINGS

- THE SUSTAINABLE EARNINGS WORKSHEET

- ROLE OF THE SUSTAINABLE EARNINGS BASE

- APPLICATION OF THE SUSTAINABLE EARNINGS BASE WORKSHEET: BAKER HUGHES INC.

- THE BAKER HUGHES WORKSHEET ANALYSIS

- SOME FURTHER POINTS ON THE BAKER HUGHES WORKSHEET